3 Reasons Why The February Inflation Data Can Worsen the Bank Run Situation

The US Bureau of Labor Statistics (BLI) just released the February Consumer Price Index (CPI) data early today (Wednesday), the 15th of March. It is perhaps the single most instrumental data in determining the US Federal Reserve's (Fed) short to medium-term monetary policy, as it represents a definitive and objective representation of the most recent inflation situation in the world's biggest economy.

**February Inflation Summary:

**

CPI: [MoM: +0.4%; Effective YoY: 6%]

Core CPI: [MoM: +0.5%; Effective YoY: 5.5%]

Interpretation: Tops Estimates But Within Expectations

As shown, inflation is still a whopping 400 basis points away from the Fed's target of 2%. Thus, despite reports that Fed will likely halt its rate hike this month due to Silicon Valley Bank's (SBV) recent collapse, which was simultaneously the second-largest bank run in US history, the continued rise in inflation will most likely invalidate earlier reports as the US central bank itself made publicly known its priority of anchoring inflation close to its target in the expense of further economic strain caused by its continued tightening.

Hence, in this article, we will cover the three fundamental reasons, together with their respective "worst-case" scenarios, why the February inflation data can potentially aggravate the "bank run situation" in the US:

1. Lower Confidence in the Banking System

First and foremost, an elevated inflation level during this time can lead to further reducing confidence in the banking system as a whole. As individuals worry that their savings are losing value due to inflation, they may start to doubt the safety of their deposits, especially upon seeing how they could end up like SBV's esteemed clients. This will cause individuals and institutions to withdraw their funds and look for more "traditional" ways to preserve their wealth, such as investing in gold or other alternative assets.

Thus, as more people withdraw their deposits, banks may experience a "liquidity crunch," making it difficult to meet the demand for withdrawals on a timely basis. If this situation continues, it can lead to a vicious cycle (downward spiral) of bank runs, further eroding confidence in the banking system.

2. Lower Real Interest Rates

Simply put, the real interest rate is the rate of interest a saver, lender, or investor receives (or expects to receive) after allowing for inflation. An elevated inflation rate can and will cause real interest rates to drop, making it less attractive for people to hold deposits in banks.

In other words, when inflation rates rise, nominal interest rates (the interest rate before accounting for inflation) do not rise as quickly (in fact, it often lags behind), leading to a decrease in real interest rates. Consequently, as people withdraw their deposits from banks, banks may find it harder to lend money to businesses and individuals, leading to decreased lending activity. Again, this further strains the banking system and contributes to the potential for bank runs.

3. Decrease in Bank Capitalization

Lastly, inflation can also cause a decrease in the value of assets, which can negatively impact bank capitalization. As the value of assets drops, banks may find it harder to maintain adequate levels of capitalization, making them more vulnerable to economic shocks (both domestic and international).

Banks becoming more susceptible can increase the likelihood of a bank run as individuals seek to withdraw their savings from potentially unstable institutions. Furthermore, this can create a self-reinforcing cycle of economic stagnation and a massive decline in banking system confidence.

Conclusion

In a nutshell, the February inflation data highlights the unwavering concerns regarding continued high inflation in the US. The potential for reduced confidence in the banking system, lower real interest rates, and decreased bank capitalization can all contribute to the potential stream of upcoming bank runs. As such, it is critical for banks to carefully manage their operations and ensure they have adequate levels of liquidity and solvency, as well as a dependable risk management setup to weather these potential storms.

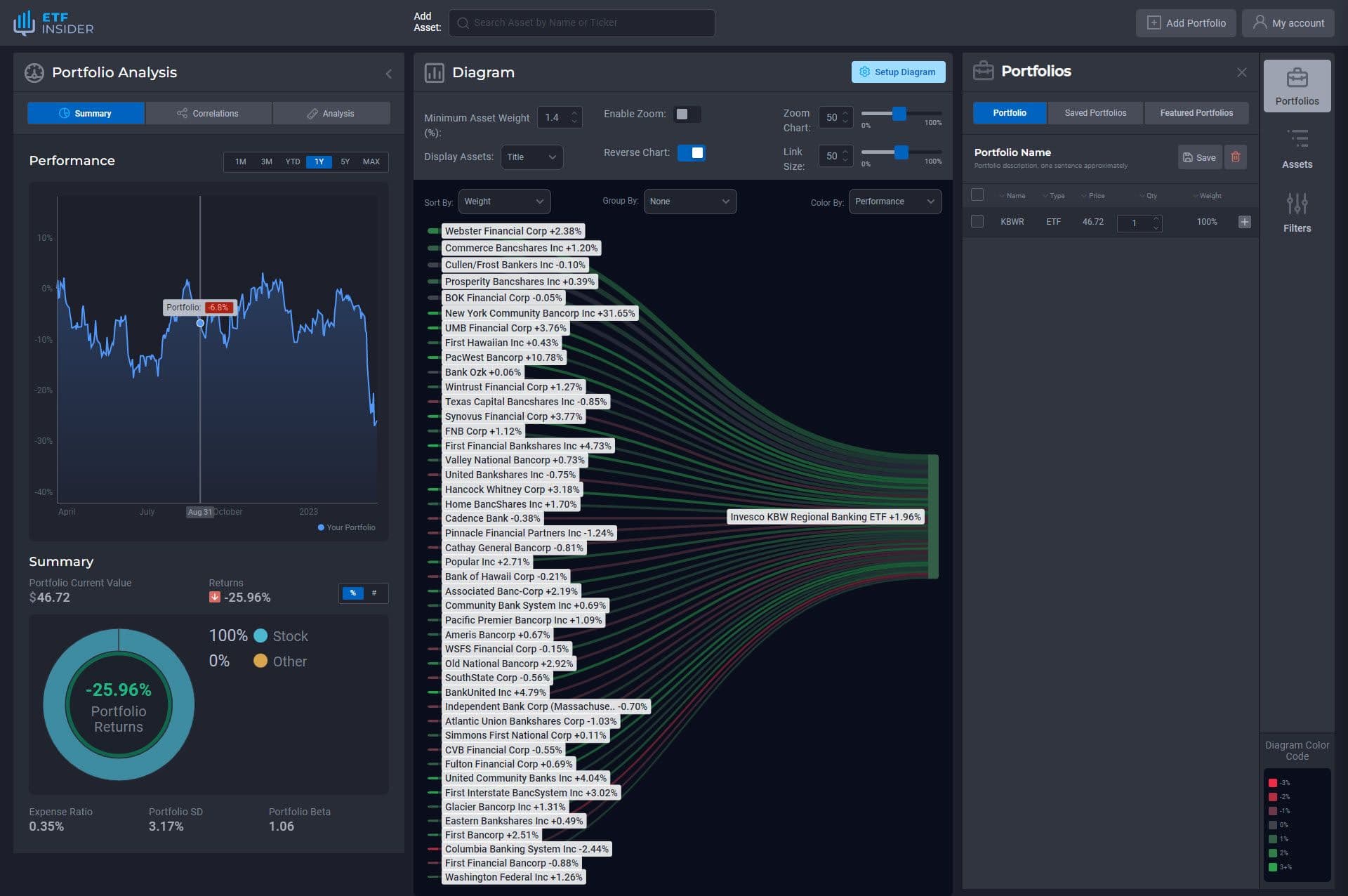

February Inflation 2.jpg

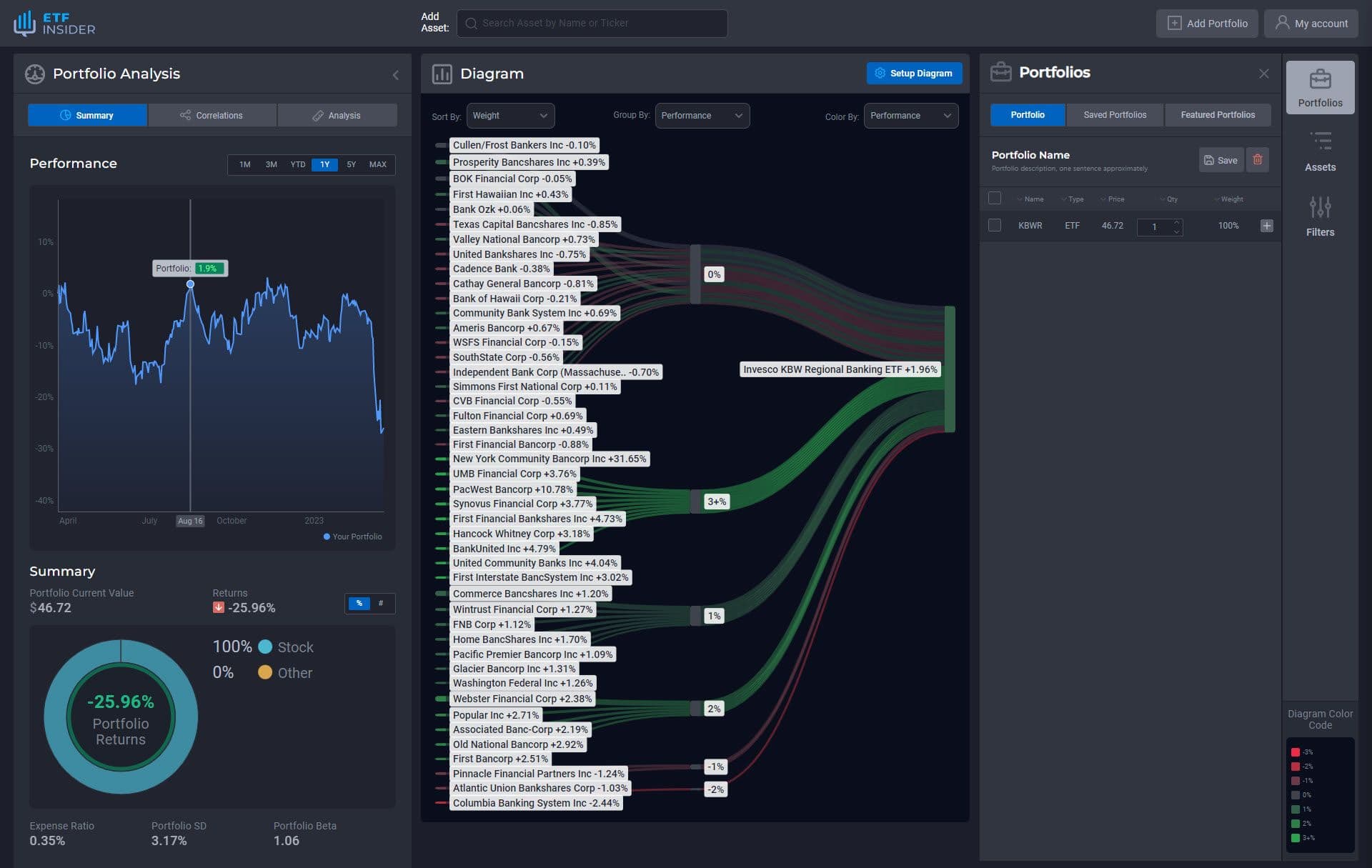

February Inflation 2.jpg

Nevertheless, for us individual investors, we can now take full advantage of sophisticated data visualization tools such as ETF Insider to do our due diligence and identify specific holdings and their corresponding weight to a particular fund (like a banking industry ETF). This helps us avoid fund overlap, overexposure to a specific stock and industry, and false diversification to ultimately optimize your long-term investment journey.

Get started